点赞、关注再看,养成良好习惯

Life is short, U need Python

初学量化投资实战,[快来点我吧]

配对交易策略实战—协整法

基本流程

配对组合 --> 计算价差 --> 决策标准 --> 确定头寸 --> 平仓获利

-

案例描述

- 本案例以上证50股票数据为对象、以协整模型为方法、以Python语言为工具进行配对交易策略的实证分析。在实证分析的过程中,主要借助于 arch 和 statsmodels等第三方库单位根检验和协整检验,进而选取股票对;然后设置决策标准和交易头寸进行回测交易。

-

数据集

- 上证50:sh50_stock_data.csv

-

导入模块

import pandas as pd

import numpy as npimport matplotlib.pyplot as plt

plt.rcParams['font.sans-serif'] = ['SimHei'] # 字体设置

import matplotlib

matplotlib.rcParams['axes.unicode_minus']=False # 负号显示问题from arch.unitroot import ADF # pip install arch

import statsmodels.api as sm

- 导入数据

sh = pd.read_csv('sh50_stock_data.csv',index_col='Trddt')

sh.index = pd.to_datetime(sh.index)

- 形成期:协整检验

# 提取数据

P_zhonghang = sh['601988'] # 中国银行

P_pufa = sh['600000'] # 浦发银行

# 设置形成期

formStart = '2014-01-01'

formEnd = '2015-01-01'P_zhonghang_f = P_zhonghang[formStart:formEnd]

P_pufa_f = P_pufa[formStart:formEnd]

# 形成期:协整关系检验

# 中国银行(A)一阶单整检验

log_P_zhonghang_f = np.log(P_zhonghang_f)adf_zhonghang = ADF(log_P_zhonghang_f)print(adf_zhonghang.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic 3.409

P-value 1.000

Lags 12

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

# 形成期:差分后的协整检验

adf_zhonghang_diff = ADF(log_P_zhonghang_f.diff()[1:])print(adf_zhonghang_diff.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic -4.571

P-value 0.000

Lags 11

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

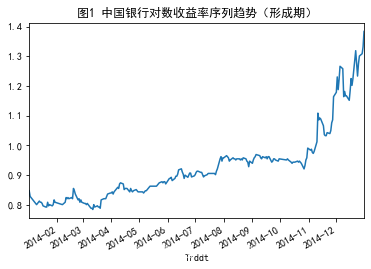

# 形成期:对数序列可视化

log_P_zhonghang_f.plot()plt.title('图1 中国银行对数收益率序列趋势(形成期)')plt.show()

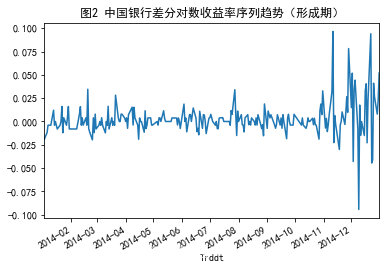

# 形成期:差分对数序列可视化

log_P_zhonghang_f.diff()[1:].plot()plt.title('图2 中国银行差分对数收益率序列趋势(形成期)')plt.show()

# 形成期:协整关系检验

# 浦发银行(B)一阶单整检验

log_P_pufa_f = np.log(P_pufa_f)adf_pufa = ADF(log_P_pufa_f)print(adf_pufa.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic 2.392

P-value 0.999

Lags 12

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

# 形成期:差分后的协整检验

adf_pufa_diff = ADF(log_P_pufa_f.diff()[1:])print(adf_pufa_diff.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic -3.888

P-value 0.002

Lags 11

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

# 形成期:对数序列可视化

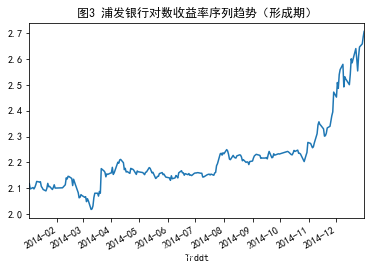

log_P_pufa_f.plot()plt.title('图3 浦发银行对数收益率序列趋势(形成期)')plt.show()

# 形成期:差分对数序列可视化

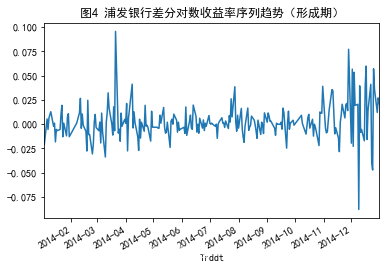

log_P_pufa_f.diff()[1:].plot()plt.title('图4 浦发银行差分对数收益率序列趋势(形成期)')plt.show()

- 形成期:股票对的回归方程(协整模型)

model = sm.OLS(log_P_pufa_f,sm.add_constant(log_P_zhonghang_f))result = model.fit()print(result.summary())

OLS Regression Results

==============================================================================

Dep. Variable: 600000 R-squared: 0.949

Model: OLS Adj. R-squared: 0.949

Method: Least Squares F-statistic: 4560.

Date: Fri, 20 Nov 2020 Prob (F-statistic): 1.83e-159

Time: 10:59:05 Log-Likelihood: 509.57

No. Observations: 245 AIC: -1015.

Df Residuals: 243 BIC: -1008.

Df Model: 1

Covariance Type: nonrobust

==============================================================================coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 1.2269 0.015 83.071 0.000 1.198 1.256

601988 1.0641 0.016 67.531 0.000 1.033 1.095

==============================================================================

Omnibus: 19.538 Durbin-Watson: 0.161

Prob(Omnibus): 0.000 Jarque-Bera (JB): 13.245

Skew: 0.444 Prob(JB): 0.00133

Kurtosis: 2.286 Cond. No. 15.2

==============================================================================Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.D:\Anaconda3\lib\site-packages\numpy\core\fromnumeric.py:2389: FutureWarning: Method .ptp is deprecated and will be removed in a future version. Use numpy.ptp instead.return ptp(axis=axis, out=out, **kwargs)

# 设置alpha、beta(交易头寸,即投资比例)

alpha = result.params[0]

beta = result.params[1]

- 形成期:残差单位根检验(残差序列为价格差序列)

# 回归方程(形成期)

spread_f = log_P_pufa_f - beta * log_P_zhonghang_f - alphaadfSpread = ADF(spread_f)print(adfSpread.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic -3.193

P-value 0.020

Lags 0

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

# 计算协整方程中残差序列的均值、方差

mu = np.mean(spread_f)

sd = np.std(spread_f)

- 构造Pair Trading类(封装协整检验)

# 构建类(协整检验)

class PairTrading:# 形成期的协整检验(形成期协整方程残差的ADF检验)def cointegration(self,priceX,priceY):log_priceX = np.log(priceX)log_priceY = np.log(priceY)results = sm.OLS(log_priceY,sm.add_constant(log_priceX)).fit()resid = results.residadfSpread = ADF(resid)if adfSpread.pvalue >= 0.05:print('''交易价格不具有协整关系.P-value of ADF test: %fCoefficients of regression:Intercept: %fBeta: %f''' % (adfSpread.pvalue, results.params[0], results.params[1]))return(None)else:print('''交易价格具有协整关系.P-value of ADF test: %fCoefficients of regression:Intercept: %fBeta: %f''' % (adfSpread.pvalue, results.params[0], results.params[1]))return(results.params[0], results.params[1])# 根据形成期的协整方程系数构造交易期协整方程,进而计算交易期协整残差序列:Co_Spread_Tradedef CointegrationSpread(self,priceX,priceY,formStart,formEnd,tradeStart,tradeEnd): formX = priceX[formStart:formEnd]formY = priceY[formStart:formEnd]tradeX = priceX[tradeStart:tradeEnd]tradeY = priceY[tradeStart:tradeEnd]coefficients = self.cointegration(formX,formY)if coefficients is None:print('未形成协整关系,无法配对.')else:spread = np.log(tradeY) - coefficients[0] - coefficients[1] * np.log(tradeX)return(spread)# 计算形成期的最优策略阈值:UpperBound 和 LowerBound,作为交易期的策略阈值def Cointegration_calBound(self,priceX,priceY,formStart,formEnd,width):spread = self.CointegrationSpread(priceX,priceY,formStart,formEnd,formStart,formEnd)mu = np.mean(spread)sd = np.std(spread)UpperBound = mu + width * sdLowerBound = mu - width * sdreturn(UpperBound,LowerBound)

# 设定交易期

tradeStart = '2015-01-01'

tradeEnd = '2015-06-30'

# 选取标的

price_zhonghang = sh['601988']

price_pufa = sh['600000']

# 形成期标的价格

price_zhonghang_f = price_zhonghang[formStart:formEnd]

price_pufa_f = price_pufa[formStart:formEnd]

# 类的实例化

pt = PairTrading() # 调用类PairTrading()

# 协整关系的系数(形成期)

coefficients = pt.cointegration(price_zhonghang_f,price_pufa_f)

交易价格具有协整关系.P-value of ADF test: 0.020415Coefficients of regression:Intercept: 1.226852Beta: 1.064103

# 形成期:价差序列

CoSpreadForm = pt.CointegrationSpread(price_zhonghang,price_pufa,formStart,formEnd,formStart,formEnd)

交易价格具有协整关系.P-value of ADF test: 0.020415Coefficients of regression:Intercept: 1.226852Beta: 1.064103

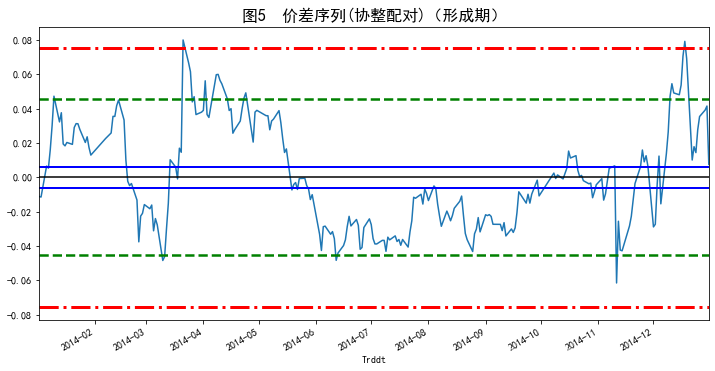

# 绘制价差序列图(形成期)

plt.figure(figsize=(12,6))CoSpreadForm.plot()plt.title('图5 价差序列(协整配对)(形成期)',loc='center', fontsize=16)plt.axhline(y=mu,color='black')

plt.axhline(y=mu+0.2*sd,color='blue',ls='-',lw=2)

plt.axhline(y=mu-0.2*sd,color='blue',ls='-',lw=2)

plt.axhline(y=mu+1.5*sd,color='green',ls='--',lw=2.5)

plt.axhline(y=mu-1.5*sd,color='green',ls='--',lw=2.5)

plt.axhline(y=mu+2.5*sd,color='red',ls='-.',lw=3)

plt.axhline(y=mu-2.5*sd,color='red',ls='-.',lw=3) plt.show()

# 交易期:价差序列

CoSpreadTrade = pt.CointegrationSpread(price_zhonghang,price_pufa,formStart,formEnd,tradeStart,tradeEnd)

交易价格具有协整关系.P-value of ADF test: 0.020415Coefficients of regression:Intercept: 1.226852Beta: 1.064103

# 根据形成期协整配对后价差序列得到的阈值

bound = pt.Cointegration_calBound(price_zhonghang,price_pufa,formStart,formEnd,width=1.5)

交易价格具有协整关系.P-value of ADF test: 0.020415Coefficients of regression:Intercept: 1.226852Beta: 1.06410

- 交易期:回测检验

# 提取交易期标的数据

P_zhonghang_t = P_zhonghang[tradeStart:tradeEnd]

P_pufa_t = P_pufa[tradeStart:tradeEnd]

# 计算交易期协整方程的残差序列(价差序列)

CoSpreadTrade = np.log(P_pufa_t) - beta * np.log(P_zhonghang_t) - alpha

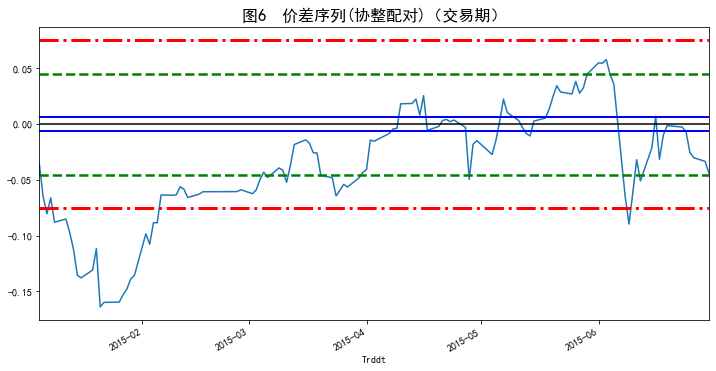

# 绘制价格区间图(交易期)

plt.figure(figsize=(12,6))CoSpreadTrade.plot()plt.title('图6 价差序列(协整配对)(交易期)',loc='center', fontsize=16)plt.axhline(y=mu,color='black')

plt.axhline(y=mu+0.2*sd,color='blue',ls='-',lw=2)

plt.axhline(y=mu-0.2*sd,color='blue',ls='-',lw=2)

plt.axhline(y=mu+1.5*sd,color='green',ls='--',lw=2.5)

plt.axhline(y=mu-1.5*sd,color='green',ls='--',lw=2.5)

plt.axhline(y=mu+2.5*sd,color='red',ls='-.',lw=3)

plt.axhline(y=mu-2.5*sd,color='red',ls='-.',lw=3) plt.show()

- 设置策略区间

# 设置触发区间:t_0=0.2; t_1=1.5; t_2=2.5

level = (float('-inf'),mu-2.5*sd,mu-1.5*sd,mu-0.2*sd,mu+0.2*sd,mu+1.5*sd,mu+2.5*sd,float('inf'))

# 把交易期的价差序列按照触发区间标准分类【-3,+3】

prcLevel = pd.cut(CoSpreadTrade,level,labels=False)-3 #剪切函数pd.cut()

pandas.cut: pandas.cut(x, bins, right=True, labels=None,

retbins=False, precision=3, include_lowest=False)参数:

- (1) x,类array对象,且必须为一维,待切割的原形式

- (2) bins, 整数、序列尺度、或间隔索引。如果bins是一个整数,它定义了x宽度范围内的等宽面元数量,但是在这种情况下,x的范围在每个边上被延长1%,以保证包括x的最小值或最大值。如果bin是序列,它定义了允许非均匀bin宽度的bin边缘。在这种情况下没有x的范围的扩展。

- (3) right,布尔值。是否是左开右闭区间

- (4) labels,用作结果箱的标签。必须与结果箱相同长度。如果FALSE,只返回整数指标面元(区间位置,即第几个区间,注意以0位置开始)。

- (5) retbins,布尔值。是否返回面元

- (6) precision,整数。返回面元的小数点几位

- (7) include_lowest,布尔值。第一个区间的左端点是否包含 返回值:

- 若labels为False则返回整数填充的Categorical(分类)或数组或Series(序列)

- 若retbins为True还返回用浮点数填充的N维数组

- 构造交易信号函数

# 构造交易信号函数

def TradeSig(prcLevel):n = len(prcLevel)signal = np.zeros(n)for i in range(1,n):if prcLevel[i-1] == 1 and prcLevel[i] == 2: # 价差从1区上穿2区,反向建仓signal[i] = -2elif prcLevel[i-1] == 1 and prcLevel[i] == 0: # 价差从1区下穿0区,平仓signal[i] = 2elif prcLevel[i-1] == 2 and prcLevel[i] == 3: # 价差从2区上穿3区,即突破3区,平仓signal[i] = 3elif prcLevel[i-1] == -1 and prcLevel[i] == -2: # 价差从-1区下穿-2区,正向建仓signal[i] = 1elif prcLevel[i-1] == -1 and prcLevel[i] == 0: # 价差从-1区上穿0区,平仓signal[i] = -1elif prcLevel[i-1] == -2 and prcLevel[i] == -3: # 价差从-2区下穿-3区,即突破-3区,平仓signal[i] = -3return(signal)

# 设置每个每天的交易信号

signal = TradeSig(prcLevel)

position = [signal[0]]

ns = len(signal)

# 设置每天开仓、平仓指令

for i in range(1,ns):position.append(position[-1])if signal[i] == 1:position[i] = 1 # 价差从-1区下穿-2区,正向建仓: 买B卖A <------(价差为B-A)elif signal[i] == -2:position[i] = -1 # 价差从1区上穿2区,反向建仓:卖B买A <------(价差为B-A)elif signal[i] == -1 and position[i-1] == 1:position[i] = 0 # 平仓elif signal[i] == 2 and position[i-1] == -1:position[i] = 0 # 平仓elif signal[i] == 3:position[i] = 0 # 平仓elif signal[i] == -3:position[i] = 0 # 平仓

position = pd.Series(position, index=CoSpreadTrade.index)

# 构造交易模拟函数

def TradeSim(priceX,priceY,position):n = len(position)size = 1000 # 因为浦发银行价格15左右,1000股对应15000,10%—20%保证金即:初始资金cash=1500-3000shareY = size * positionshareX = [(-beta) * shareY[0] * priceY[0] / priceX[0]] # CoSpreadT = np.log(PBt)-beta*np.log(PAt)-alphacash = [2000]for i in range(1,n):shareX.append(shareX[i-1])cash.append(cash[i-1])if position[i-1] == 0 and position[i] == 1:shareX[i] = (-beta)*shareY[i]*priceY[i]/priceX[i]cash[i] = cash[i-1]-(shareY[i]*priceY[i]+shareX[i]*priceX[i])elif position[i-1] == 0 and position[i] == -1:shareX[i] = (-beta)*shareY[i]*priceY[i]/priceX[i]cash[i] = cash[i-1]-(shareY[i]*priceY[i]+shareX[i]*priceX[i])elif position[i-1] == 1 and position[i] == 0:shareX[i] = 0cash[i] = cash[i-1]+(shareY[i-1]*priceY[i]+shareX[i-1]*priceX[i])elif position[i-1] == -1 and position[i] == 0:shareX[i] = 0cash[i] = cash[i-1]+(shareY[i-1]*priceY[i]+shareX[i-1]*priceX[i])cash = pd.Series(cash,index=position.index)shareY = pd.Series(shareY,index=position.index)shareX = pd.Series(shareX,index=position.index)asset = cash + shareY*priceY + shareX*priceXaccount = pd.DataFrame({'Position':position,'ShareY':shareY,'ShareX':shareX,'Cash':cash,'Asset':asset})return(account)

account = TradeSim(P_zhonghang_t,P_pufa_t,position)

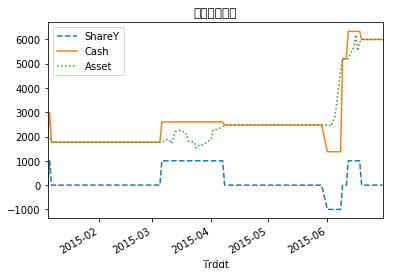

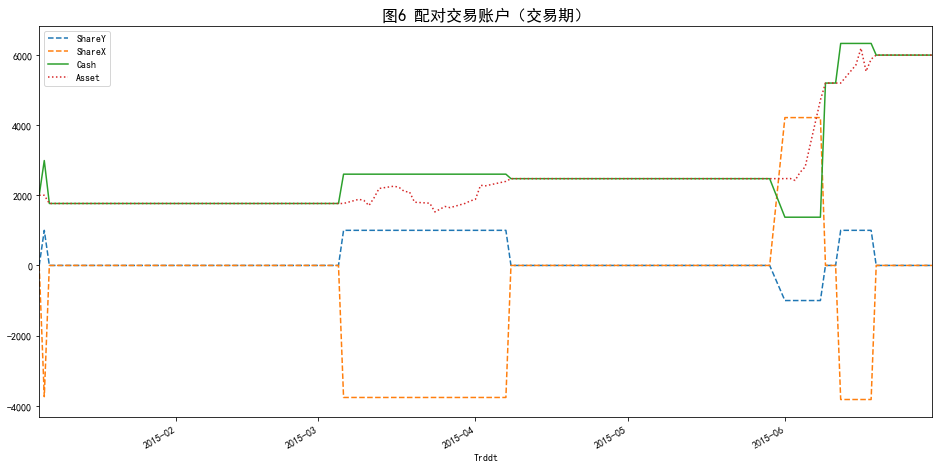

account.iloc[:, [1,2,3,4]].plot(style=['--','--','-',':'], figsize=(16,8))plt.title('图6 配对交易账户(交易期)',loc='center', fontsize=16) plt.show()

其中,(1)ShareY 可以表示配对仓位(1000倍)(正反向持仓与不持仓);(2)ShareX 表示对应配对仓位(1000倍)(反正向持仓与不持仓);(3)Cash 曲线表示现金的变化,初始现金为2000元;(4)Asset 曲线表示资产的变化。

结论:

-

观察交易仓位曲线图,可以看出自2015年1月1日到2015年6月底期间,配对交易信号触发不多(计4次)。

-

观察现金曲线图,由于开仓可能需要现金,现金曲线有升有降,而第三次平仓之后获利很多,现金曲线大幅上涨,到6月底,现金部位达到了5992.514元。

-

再观察资产曲线图,配对资产整体呈现上升趋势,资产由2000元转变成5992.514元。

-

整体而言,对中国银行和浦发银行两只股票进行配对交易的策略绩效表现不错。

-

构造Back Testing类(封装回测检验)

class BackTesting: # 构造交易信号函数def TradeSigPosition(self,CoSpreadT,level,k):prcLevel = pd.cut(CoSpreadT,level,labels=False)-kn = len(prcLevel)signal = np.zeros(n)for i in range(1,n):if prcLevel[i-1] == 1 and prcLevel[i] == 2: # 价差从1区上穿2区,反向建仓signal[i] = -2elif prcLevel[i-1] == 1 and prcLevel[i] == 0: # 价差从1区下穿0区,平仓signal[i] = 2elif prcLevel[i-1] == 2 and prcLevel[i] == 3: # 价差从2区上穿3区,即突破3区,平仓signal[i] = 3elif prcLevel[i-1] == -1 and prcLevel[i] == -2: # 价差从-1区下穿-2区,正向建仓signal[i] = 1elif prcLevel[i-1] == -1 and prcLevel[i] == 0: # 价差从-1区上穿0区,平仓signal[i] = -1elif prcLevel[i-1] == -2 and prcLevel[i] == -3: # 价差从-2区下穿-3区,即突破-3区,平仓signal[i] = -3position = [signal[0]]ns = len(signal)# 设置每天开仓、平仓指令for i in range(1,ns):position.append(position[-1])if signal[i] == 1:position[i] = 1 # 价差从-1区下穿-2区,正向建仓: 买B卖A <------(价差为B-A)elif signal[i] == -2:position[i] = -1 # 价差从1区上穿2区,反向建仓:卖B买A <------(价差为B-A)elif signal[i] == -1 and position[i-1] == 1:position[i] = 0 # 平仓elif signal[i] == 2 and position[i-1] == -1:position[i] = 0 # 平仓elif signal[i] == 3:position[i] = 0 # 平仓elif signal[i] == -3:position[i] = 0 # 平仓position = pd.Series(position, index=CoSpreadT.index)return(position)# 构造交易模拟函数def TradeSim(self,priceX,priceY,position,size,cash):n = len(position)

# size = 1000 # 因为浦发银行价格15左右,1000股对应15000,10%—20%保证金即:初始资金cash=1500-3000shareY = size * positionshareX = [(-beta) * shareY[0] * priceY[0] / priceX[0]] # CoSpreadT = np.log(PBt)-beta*np.log(PAt)-alpha# cash = [2000]for i in range(1,n):shareX.append(shareX[i-1])cash.append(cash[i-1])if position[i-1] == 0 and position[i] == 1:shareX[i] = (-beta)*shareY[i]*priceY[i]/priceX[i]cash[i] = cash[i-1]-(shareY[i]*priceY[i]+shareX[i]*priceX[i])elif position[i-1] == 0 and position[i] == -1:shareX[i] = (-beta)*shareY[i]*priceY[i]/priceX[i]cash[i] = cash[i-1]-(shareY[i]*priceY[i]+shareX[i]*priceX[i])elif position[i-1] == 1 and position[i] == 0:shareX[i] = 0cash[i] = cash[i-1]+(shareY[i-1]*priceY[i]+shareX[i-1]*priceX[i])elif position[i-1] == -1 and position[i] == 0:shareX[i] = 0cash[i] = cash[i-1]+(shareY[i-1]*priceY[i]+shareX[i-1]*priceX[i])cash = pd.Series(cash,index=position.index)shareY = pd.Series(shareY,index=position.index)shareX = pd.Series(shareX,index=position.index)asset = cash + shareY*priceY + shareX*priceXaccount = pd.DataFrame({'Position':position,'ShareY':shareY,'ShareX':shareX,'Cash':cash,'Asset':asset})return(account)

bt = BackTesting()position = bt.TradeSigPosition(CoSpreadTrade,level,3)account = bt.TradeSim(P_zhonghang_t,P_pufa_t,position,1000,[2000])account.iloc[:, [1,2,3,4]].plot(style=['--','--','-',':'], figsize=(16,8))

plt.title('配对交易账户(交易期)',loc='center', fontsize=16)

plt.show()

参考资料:

- 蔡立耑. 量化投资以Python为工具[M]. 北京:电子工业出版社,2017.

数据下载

- 链接:https://pan.baidu.com/s/1nIFSnTzhTJk2ETh0bJ_SkA

提取码:8gy4

- 写作不易,切勿白剽

- 博友们的点赞和关注就是对博主坚持写作的最大鼓励

- 持续更新,未完待续…