配对交易的步骤

1. 如何挑选进行配对的股票

2. 挑选好股票对以后,如何制定交易策略,开仓点如何设计

3. 开仓是,两只股票如何进行多空仓对比

股票对的选择

1. 行业内匹配

2. 产业链配对

3. 财务管理配对

最小距离法

配对交易需要对股票价格进行标准化处理。假设 P t i ( t = 0 , 1 , 2 , . . . , T ) P_t^i(t=0,1,2,...,T) Pti(t=0,1,2,...,T)表示股票i在第t天的价格,那么股票i在第t天的单期收益率可以表达为:

r t i = P t i − P t − 1 i P t − 1 i , t = 1 , 2 , 3 , . . . , T r_t^i=\frac{P_t^i-P_{t-1}^{i}}{P_{t-1}^{i}},t=1,2,3,...,T rti=Pt−1iPti−Pt−1i,t=1,2,3,...,T

用 p ^ t i \hat{p}_t^i p^ti 表示股票i在第t天的标准化价格,学界和业界认为 p ^ t i \hat{p}_t^i p^ti可以有这t天内的累计收益率来计算:

p ^ t i = ∏ τ = 1 t ( 1 + r τ i ) \hat{p}^i_t=\prod_{\tau=1}^t (1+r_\tau^i) p^ti=∏τ=1t(1+rτi)

假设有股票X,Y,则我们可以计算二者之间的标准化价差之平方和 S S D X , Y SSD_{X,Y} SSDX,Y

S S D X , Y = ∑ t = 1 T ( p ^ t X − p ^ t Y ) 2 \\ SSD_{X,Y}=\sum_{t=1}^T (\hat{p}_t^X-\hat{p}_t^Y)^2 SSDX,Y=∑t=1T(p^tX−p^tY)2

下面使用python计算SSD

import pandas as pd

sh=pd.read_csv('sh50p.csv',index_col='Trddt')

sh.index=pd.to_datetime(sh.index)

sh.head()

| 600000 | 600010 | 600015 | 600016 | 600018 | 600028 | 600030 | 600036 | 600048 | 600050 | ... | 601688 | 601766 | 601800 | 601818 | 601857 | 601901 | 601985 | 601988 | 601989 | 601998 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Trddt | |||||||||||||||||||||

| 2010-01-04 | 9.997 | 2.260 | 6.541 | 4.627 | 4.775 | 8.445 | 17.927 | 13.174 | 6.443 | 6.703 | ... | - | 4.991 | - | - | 11.284 | - | - | 3.055 | 4.591 | 6.498 |

| 2010-01-05 | 10.072 | 2.250 | 6.706 | 4.708 | 4.783 | 8.494 | 18.804 | 13.188 | 6.243 | 6.937 | ... | - | 4.982 | - | - | 11.499 | - | - | 3.090 | 4.573 | 6.578 |

| 2010-01-06 | 9.874 | 2.255 | 6.461 | 4.615 | 4.733 | 8.311 | 18.586 | 12.913 | 6.237 | 6.787 | ... | - | 4.947 | - | - | 11.342 | - | - | 3.055 | 4.627 | 6.393 |

| 2010-01-07 | 9.652 | 2.201 | 6.328 | 4.493 | 4.602 | 8.091 | 18.133 | 12.578 | 6.240 | 6.590 | ... | - | 4.875 | - | - | 11.267 | - | - | 2.998 | 4.573 | 6.176 |

| 2010-01-08 | 9.761 | 2.211 | 6.370 | 4.539 | 4.618 | 8.005 | 18.483 | 12.578 | 6.322 | 6.674 | ... | - | 4.902 | - | - | 11.135 | - | - | 3.012 | 4.525 | 6.232 |

5 rows × 50 columns

# 定义配对形成期

formStart='2014-01-01'

formEnd='2015-01-01'

# 形成期数据

shform=sh[formStart:formEnd]

shform.head(2)

| 600000 | 600010 | 600015 | 600016 | 600018 | 600028 | 600030 | 600036 | 600048 | 600050 | ... | 601688 | 601766 | 601800 | 601818 | 601857 | 601901 | 601985 | 601988 | 601989 | 601998 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Trddt | |||||||||||||||||||||

| 2014-01-02 | 8.307 | 2.360 | 6.371 | 6.183 | 5.031 | 4.117 | 12.288 | 9.719 | 5.156 | 3.146 | ... | 8.534 | 4.869 | 3.781 | 2.383 | 7.245 | 5.91 | - | 2.333 | 5.617 | 3.634 |

| 2014-01-03 | 8.138 | 2.594 | 6.187 | 6.087 | 4.906 | 4.043 | 11.937 | 9.520 | 5.112 | 3.088 | ... | 8.293 | 4.791 | 3.725 | 2.356 | 7.217 | 5.91 | - | 2.289 | 5.517 | 3.578 |

2 rows × 50 columns

# 提取中国银行 601988 的收盘价数据

PAf=shform['601988']

# 提取浦发银行 600000 的收盘价数据

PBf = shform['600000']

#合并两只股票

pairf=pd.concat([PAf,PBf],axis=1)

len(pairf)

245

import numpy as np

# 构造标准化价格之差平方累计SSD函数

def SSD(priceX,priceY):if priceX is None or priceY is None:print('缺少价格序列')returnX = (priceX-priceX.shift(1))/priceX.shift(1)[1:]returnY = (priceY-priceY.shift(1))/priceY.shift(1)[1:]standardX=(returnX+1).cumprod()standardY=(returnY+1).cumprod()SSD = np.sum((standardX-standardY)**2)return SSD

dis=SSD(PAf,PBf)

dis

0.47481704588389073

SSD_rst=[]

for i in shform.columns:for j in shform.columns:if i==j:continue;A=shform[i]B=shform[j]try:num=SSD(A,B)except:continue# print(i,j,num)try:lst=[i,j,num]except:continueSSD_rst.append(lst)

SSDdf=pd.DataFrame(SSD_rst)

SSDdf.head()

| 0 | 1 | 2 | |

|---|---|---|---|

| 0 | 600000 | 600010 | 7.366730 |

| 1 | 600000 | 600015 | 0.668806 |

| 2 | 600000 | 600016 | 2.563524 |

| 3 | 600000 | 600018 | 7.823916 |

| 4 | 600000 | 600028 | 3.976679 |

SSDdf.sort_values(by=2)

| 0 | 1 | 2 | |

|---|---|---|---|

| 102 | 600015 | 601166 | 0.245662 |

| 977 | 601166 | 600015 | 0.245662 |

| 1435 | 601857 | 601398 | 0.329987 |

| 1244 | 601398 | 601857 | 0.329987 |

| 387 | 600050 | 601988 | 0.422743 |

| 1452 | 601988 | 600050 | 0.422743 |

| 984 | 601166 | 600050 | 0.446014 |

| 375 | 600050 | 601166 | 0.446014 |

| 1443 | 601988 | 600000 | 0.474817 |

| 36 | 600000 | 601988 | 0.474817 |

| 300 | 600036 | 601318 | 0.485505 |

| 1099 | 601318 | 600036 | 0.485505 |

| 1445 | 601988 | 600015 | 0.519690 |

| 114 | 600015 | 601988 | 0.519690 |

| 982 | 601166 | 600036 | 0.533362 |

| 297 | 600036 | 601166 | 0.533362 |

| 353 | 600050 | 600015 | 0.545751 |

| 86 | 600015 | 600050 | 0.545751 |

| 1011 | 601166 | 601988 | 0.546044 |

| 1468 | 601988 | 601166 | 0.546044 |

| 1002 | 601166 | 601318 | 0.568370 |

| 1117 | 601318 | 601166 | 0.568370 |

| 303 | 600036 | 601398 | 0.653760 |

| 1216 | 601398 | 600036 | 0.653760 |

| 948 | 601088 | 600111 | 0.656164 |

| 491 | 600111 | 601088 | 0.656164 |

| 78 | 600015 | 600000 | 0.668806 |

| 1 | 600000 | 600015 | 0.668806 |

| 381 | 600050 | 601398 | 0.704233 |

| 1218 | 601398 | 600050 | 0.704233 |

| ... | ... | ... | ... |

| 479 | 600111 | 600109 | 64.595128 |

| 440 | 600109 | 600111 | 64.595128 |

| 1434 | 601857 | 601390 | 65.941405 |

| 1205 | 601390 | 601857 | 65.941405 |

| 947 | 601088 | 600109 | 67.396051 |

| 452 | 600109 | 601088 | 67.396051 |

| 1186 | 601390 | 600585 | 71.932721 |

| 653 | 600585 | 601390 | 71.932721 |

| 1204 | 601390 | 601766 | 72.876730 |

| 1395 | 601766 | 601390 | 72.876730 |

| 1174 | 601390 | 600018 | 73.037316 |

| 185 | 600018 | 601390 | 73.037316 |

| 689 | 600637 | 601186 | 75.475072 |

| 1070 | 601186 | 600637 | 75.475072 |

| 674 | 600637 | 600109 | 78.702164 |

| 445 | 600109 | 600637 | 78.702164 |

| 965 | 601088 | 601390 | 79.636906 |

| 1194 | 601390 | 601088 | 79.636906 |

| 1182 | 601390 | 600111 | 81.322417 |

| 497 | 600111 | 601390 | 81.322417 |

| 809 | 600887 | 601390 | 82.309679 |

| 1190 | 601390 | 600887 | 82.309679 |

| 1067 | 601186 | 600518 | 87.971590 |

| 572 | 600518 | 601186 | 87.971590 |

| 442 | 600109 | 600518 | 96.995893 |

| 557 | 600518 | 600109 | 96.995893 |

| 692 | 600637 | 601390 | 97.687461 |

| 1187 | 601390 | 600637 | 97.687461 |

| 1184 | 601390 | 600518 | 111.693514 |

| 575 | 600518 | 601390 | 111.693514 |

1560 rows × 3 columns

协整模型

协整模型指如果X股票的对数价格是非平稳时间序列,且对数价格的差分序列是平稳的,责成X股票的对数价格是一阶单整序列。

又 l o g ( P t X ) − l o g ( P t − 1 X ) = l o g ( P t X P t − 1 X ) = l o g ( 1 + r t X ) = r t X log(P_t^X)-log(P_{t-1}^X)=log(\frac{P_t^X}{P_{t-1}^X}) \\=log(1+r_t^X) \\~=r_t^X log(PtX)−log(Pt−1X)=log(Pt−1XPtX)=log(1+rtX) =rtX

下面计算中国银行和浦发银行是否是一阶单整序列

from arch.unitroot import ADF

import numpy as np

PAf.head()

Trddt

2014-01-02 2.333

2014-01-03 2.289

2014-01-06 2.262

2014-01-07 2.253

2014-01-08 2.244

Name: 601988, dtype: float64

PAflog=np.log(PAf)

adfA=ADF(PAflog)

print(adfA.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic 3.409

P-value 1.000

Lags 12

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

统计量较大,我们接受原假设,原序列存在单位根,所以中国银行的收盘价的对数序列是非平稳序列

#对数差分

retA=PAflog.diff()[1:]

retA.head()

Trddt

2014-01-03 -0.019040

2014-01-06 -0.011866

2014-01-07 -0.003987

2014-01-08 -0.004003

2014-01-09 -0.004019

Name: 601988, dtype: float64

adfretA=ADF(retA)

print(adfretA.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic -4.571

P-value 0.000

Lags 11

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

统计量较小,所以我们拒绝原假设,对数差分序列没有单位根,所以中国银行的对数差分序列是平稳序列

由此说明中国银行的对数价格序列是一阶单整序列

# 对浦发银行进行检验

PBflog=np.log(PBf)

adfB=ADF(PBflog)

print(adfB.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic 2.392

P-value 0.999

Lags 12

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

统计量较大,我们接受原假设,原序列存在单位根,所以浦发银行的收盘价的对数序列是非平稳序列

#对数差分序列

retB = PBflog.diff()[1:]

adfretB=ADF(retB)

print(adfretB.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic -3.888

P-value 0.002

Lags 11

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

统计量较小,所以拒绝原假设,不存在单位根,所以浦发银行的对数差分序列是平稳序列

由此说明浦发银行的对数序列是一阶单整序列

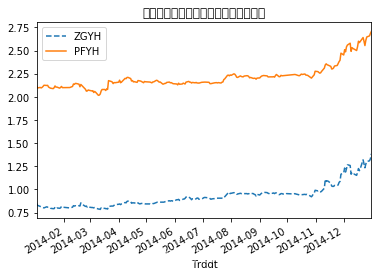

#绘制对数时序图

import matplotlib.pyplot as plt

PAflog.plot(label='ZGYH',style='--')

PBflog.plot(label='PFYH',style='-')

plt.legend(loc='upper left')

plt.title("中国银行和浦发银行的对数价格时序图")

Text(0.5, 1.0, '中国银行和浦发银行的对数价格时序图')

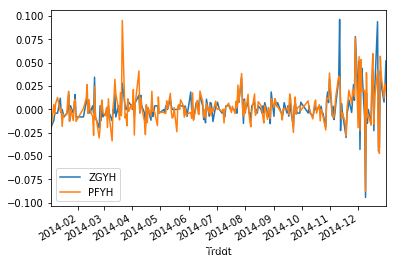

retA.plot(label='ZGYH')

retB.plot(label='PFYH')

plt.legend(loc='lower left')

<matplotlib.legend.Legend at 0x1c238d0eb8>

检验两个对数序列的协整性

方式是对两个序列进行线性拟合,对残差进行检验,如果残差序列是平稳的,说明两个对数序列具有协整性

import statsmodels.api as sm

model=sm.OLS(PBflog,sm.add_constant(PAflog))

/Users/yaochenli/anaconda3/lib/python3.7/site-packages/numpy/core/fromnumeric.py:2389: FutureWarning: Method .ptp is deprecated and will be removed in a future version. Use numpy.ptp instead.return ptp(axis=axis, out=out, **kwargs)

results=model.fit()

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: 600000 R-squared: 0.949

Model: OLS Adj. R-squared: 0.949

Method: Least Squares F-statistic: 4560.

Date: Fri, 23 Aug 2019 Prob (F-statistic): 1.83e-159

Time: 17:40:05 Log-Likelihood: 509.57

No. Observations: 245 AIC: -1015.

Df Residuals: 243 BIC: -1008.

Df Model: 1

Covariance Type: nonrobust

==============================================================================coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 1.2269 0.015 83.071 0.000 1.198 1.256

601988 1.0641 0.016 67.531 0.000 1.033 1.095

==============================================================================

Omnibus: 19.538 Durbin-Watson: 0.161

Prob(Omnibus): 0.000 Jarque-Bera (JB): 13.245

Skew: 0.444 Prob(JB): 0.00133

Kurtosis: 2.286 Cond. No. 15.2

==============================================================================Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

结果比较显著

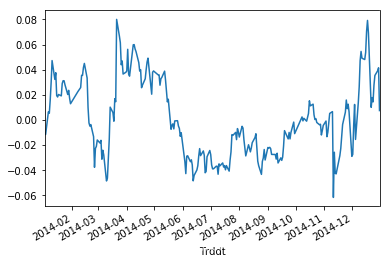

对残差进行平稳性检验

#提取回归截距

alpha=results.params[0]

beta =results.params[1]

spread=PBflog-beta*PAflog-alpha

spread.head()

Trddt

2014-01-02 -0.011214

2014-01-03 -0.011507

2014-01-06 0.006511

2014-01-07 0.005361

2014-01-08 0.016112

dtype: float64

spread.plot()

<matplotlib.axes._subplots.AxesSubplot at 0x1c23a44470>

# 价差序列单位根检验

# 因为残差的均值是0,所以trend设为nc

adfSpread=ADF(spread,trend='nc')

print(adfSpread.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic -3.199

P-value 0.001

Lags 0

-------------------------------------Trend: No Trend

Critical Values: -2.57 (1%), -1.94 (5%), -1.62 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

统计量较小,所以拒绝原假设,认为残差是平稳的

配对交易策略的制定

最小距离法

计算形成期内标准化的价格序列差 P ^ t X − P ^ t Y \hat{P}^X_t-\hat{P}^Y_t P^tX−P^tY的平均值 μ \mu μ和标准差 σ \sigma σ,设定交易信号出发点为 μ + − 2 σ \mu+-2\sigma μ+−2σ交易期为6个月。由于浦发银行和中国银行为银行业股票,价格比较稳定,因此我们设定交易期内价差超过 μ + − 1.2 σ \mu+-1.2\sigma μ+−1.2σ时触发交易信号。

#最短距离法交易策略

#中国银行的标准化价格

standardA=(1+retA).cumprod()

#浦发银行的标准化价格

standardB=(1+retB).cumprod()

#标准价差

SSD_pair=standardB-standardA

SSD_pair.head()

Trddt

2014-01-03 -0.001514

2014-01-06 0.015407

2014-01-07 0.013962

2014-01-08 0.024184

2014-01-09 0.037629

dtype: float64

meanSSD_pair = np.mean(SSD_pair)

sdSSD_pair=np.std(SSD_pair)

thresholdUP=meanSSD_pair+1.2*sdSSD_pair

thresholdDOWN=meanSSD_pair-1.2*sdSSD_pair

SSD_pair.plot()

plt.axhline(y=meanSSD_pair,color='black')

plt.axhline(y=thresholdUP,color='blue')

plt.axhline(y=thresholdDOWN,color='red')

<matplotlib.lines.Line2D at 0x1c24027860>

在交易期当价差上穿阀值的时候反向开仓,回归平均线左右的时候平仓,当价差下穿阀值线的时候正向开仓,在价差回归平均线左右的时候平仓。

#交易期

tradStart='2015-01-01'

tradEnd='2015-06-30'

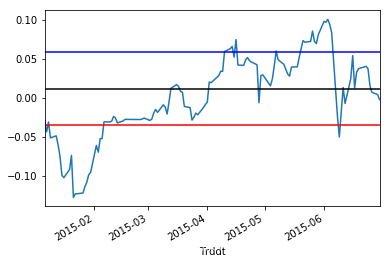

PAt=sh.loc[tradStart:tradEnd,'601988']

PBt=sh.loc[tradStart:tradEnd,'600000']

def spreadCal(x,y):retx=(x-x.shift(1))/x.shift(1)[1:]rety=(y-y.shift(1))/y.shift(1)[1:]standardX=(1+retx).cumprod()standardY=(1+rety).cumprod()spread=standardY-standardXreturn spread

TradSpread=spreadCal(PAt,PBt).dropna()

TradSpread.describe()

count 118.000000

mean 0.001064

std 0.054323

min -0.127050

25% -0.028249

50% 0.005682

75% 0.041375

max 0.100249

dtype: float64

TradSpread.plot()

plt.axhline(y=meanSSD_pair,color='black')

plt.axhline(y=thresholdUP,color='blue')

plt.axhline(y=thresholdDOWN,color='red')

<matplotlib.lines.Line2D at 0x1c240f9a58>

协整模型

构建PairTrading类

import re

import pandas as pd

import numpy as np

from arch.unitroot import ADF

import statsmodels.api as sm

class PairTrading:#计算两个股票之间的距离def SSD(self,priceX,priceY):if priceX is None or priceY is None:print('缺少价格序列')returnreturnX=(priceX-priceX.shift(1))/priceX.shift(1)[1:]returnY=(priceY-priceY.shift(1))/priceY.shift(1)[1:]standardX=(1+returnX).cumprod()standardY=(1+returnY).cumprod()SSD=np.sum((standardY-standardX)**2)return SSD#计算标准价差序列def SSDSpread(self,priceX,priceY):if priceX is None or priceY is None:print('缺少价格徐磊')returnreturnX=(priceX-priceX.shift(1))/priceX.shift(1)[1:]returnY=(priceY-priceY.shift(1))/priceY.shift(1)[1:]standardX=(1+returnX).cumprod()standardY=(1+returnY).cumprod()spread=standardY-standardXreturn spread#判断是否是协整序列,并返回协整序列的线性回归参数def cointegration(self,priceX,priceY):if priceX is None or priceY is None:print('缺少价格序列.')priceX=np.log(priceX)priceY=np.log(priceY)results=sm.OLS(priceY,sm.add_constant(priceX)).fit()resid=results.residadfSpread=ADF(resid)if adfSpread.pvalue>=0.05:print('''交易价格不具有协整关系.P-value of ADF test: %fCoefficients of regression:Intercept: %fBeta: %f''' % (adfSpread.pvalue, results.params[0], results.params[1]))return(None)else:print('''交易价格具有协整关系.P-value of ADF test: %fCoefficients of regression:Intercept: %fBeta: %f''' % (adfSpread.pvalue, results.params[0], results.params[1]))return(results.params[0], results.params[1])#计算协整序列差def CointegrationSpread(self,priceX,priceY,formPeriod,tradePeriod):if priceX is None or priceY is None:print('缺少价格序列.')if not (re.fullmatch('\d{4}-\d{2}-\d{2}:\d{4}-\d{2}-\d{2}',formPeriod)or re.fullmatch('\d{4}-\d{2}-\d{2}:\d{4}-\d{2}-\d{2}',tradePeriod)):print('形成期或交易期格式错误.')formX=priceX[formPeriod.split(':')[0]:formPeriod.split(':')[1]]formY=priceY[formPeriod.split(':')[0]:formPeriod.split(':')[1]]coefficients=self.cointegration(formX,formY)if coefficients is None:print('未形成协整关系,无法配对.')else:spread=(np.log(priceY[tradePeriod.split(':')[0]:tradePeriod.split(':')[1]])-coefficients[0]-coefficients[1]*np.log(priceX[tradePeriod.split(':')[0]:tradePeriod.split(':')[1]]))return(spread)#计算边界def calBound(self,priceX,priceY,method,formPeriod,width=1.5):if not (re.fullmatch('\d{4}-\d{2}-\d{2}:\d{4}-\d{2}-\d{2}',formPeriod)or re.fullmatch('\d{4}-\d{2}-\d{2}:\d{4}-\d{2}-\d{2}',tradePeriod)):print('形成期或交易期格式错误.')if method=='SSD':spread=self.SSDSpread(priceX[formPeriod.split(':')[0]:formPeriod.split(':')[1]],priceY[formPeriod.split(':')[0]:formPeriod.split(':')[1]]) mu=np.mean(spread)sd=np.std(spread)UpperBound=mu+width*sdLowerBound=mu-width*sdreturn(UpperBound,LowerBound)elif method=='Cointegration':spread=self.CointegrationSpread(priceX,priceY,formPeriod,formPeriod)mu=np.mean(spread)sd=np.std(spread)UpperBound=mu+width*sdLowerBound=mu-width*sdreturn(UpperBound,LowerBound)else:print('不存在该方法. 请选择"SSD"或是"Cointegration".')

formPeriod='2014-01-01:2015-01-01'

tradePeriod='2015-01-01:2015-06-30'

priceA=sh['601988']

priceB=sh['600000']

priceAf=priceA[formPeriod.split(':')[0]:formPeriod.split(':')[1]]

priceBf=priceB[formPeriod.split(':')[0]:formPeriod.split(':')[1]]

priceAt=priceA[tradePeriod.split(':')[0]:tradePeriod.split(':')[1]]

priceBt=priceB[tradePeriod.split(':')[0]:tradePeriod.split(':')[1]]

pt=PairTrading()

SSD=pt.SSD(priceAf,priceBf)

SSD

0.47481704588389073

SSDspread=pt.SSDSpread(priceAf,priceBf)

SSDspread.describe()

SSDspread.head()

Trddt

2014-01-02 NaN

2014-01-03 -0.001484

2014-01-06 0.015385

2014-01-07 0.013946

2014-01-08 0.024184

dtype: float64

coefficients=pt.cointegration(priceAf,priceBf)

coefficients

交易价格具有协整关系.P-value of ADF test: 0.020415Coefficients of regression:Intercept: 1.226852Beta: 1.064103(1.2268515742404387, 1.0641034525888144)

CoSpreadF=pt.CointegrationSpread(priceA,priceB,formPeriod,formPeriod)

CoSpreadF.head()

交易价格具有协整关系.P-value of ADF test: 0.020415Coefficients of regression:Intercept: 1.226852Beta: 1.064103Trddt

2014-01-02 -0.011214

2014-01-03 -0.011507

2014-01-06 0.006511

2014-01-07 0.005361

2014-01-08 0.016112

dtype: float64

CoSpreadTr=pt.CointegrationSpread(priceA,priceB,formPeriod,tradePeriod)

CoSpreadTr.describe()

交易价格具有协整关系.P-value of ADF test: 0.020415Coefficients of regression:Intercept: 1.226852Beta: 1.064103count 119.000000

mean -0.037295

std 0.052204

min -0.163903

25% -0.063038

50% -0.033336

75% 0.000503

max 0.057989

dtype: float64

bound=pt.calBound(priceA,priceB,'Cointegration',formPeriod,width=1.2)

bound

交易价格具有协整关系.P-value of ADF test: 0.020415Coefficients of regression:Intercept: 1.226852Beta: 1.064103(0.03627938704534019, -0.03627938704533997)

#配对交易实测

#提取形成期数据

formStart='2014-01-01'

formEnd='2015-01-01'

PA=sh['601988']

PB=sh['600000']PAf=PA[formStart:formEnd]

PBf=PB[formStart:formEnd]

#形成期协整关系检验

#一阶单整检验

log_PAf=np.log(PAf)

adfA=ADF(log_PAf)

print(adfA.summary().as_text())

adfAd=ADF(log_PAf.diff()[1:])

print(adfAd.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic 3.409

P-value 1.000

Lags 12

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.Augmented Dickey-Fuller Results

=====================================

Test Statistic -4.571

P-value 0.000

Lags 11

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

log_PBf=np.log(PBf)

adfB=ADF(log_PBf)

print(adfB.summary().as_text())

adfBd=ADF(log_PBf.diff()[1:])

print(adfBd.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic 2.392

P-value 0.999

Lags 12

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.Augmented Dickey-Fuller Results

=====================================

Test Statistic -3.888

P-value 0.002

Lags 11

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

#协整关系检验

model=sm.OLS(log_PBf,sm.add_constant(log_PAf)).fit()

model.summary()

| Dep. Variable: | 600000 | R-squared: | 0.949 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.949 |

| Method: | Least Squares | F-statistic: | 4560. |

| Date: | Fri, 23 Aug 2019 | Prob (F-statistic): | 1.83e-159 |

| Time: | 17:43:03 | Log-Likelihood: | 509.57 |

| No. Observations: | 245 | AIC: | -1015. |

| Df Residuals: | 243 | BIC: | -1008. |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | 1.2269 | 0.015 | 83.071 | 0.000 | 1.198 | 1.256 |

| 601988 | 1.0641 | 0.016 | 67.531 | 0.000 | 1.033 | 1.095 |

| Omnibus: | 19.538 | Durbin-Watson: | 0.161 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 13.245 |

| Skew: | 0.444 | Prob(JB): | 0.00133 |

| Kurtosis: | 2.286 | Cond. No. | 15.2 |

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

alpha=model.params[0]

alpha

1.2268515742404387

beta=model.params[1]

beta

1.0641034525888144

#残差单位根检验

spreadf=log_PBf-beta*log_PAf-alpha

adfSpread=ADF(spreadf)

print(adfSpread.summary().as_text())

Augmented Dickey-Fuller Results

=====================================

Test Statistic -3.193

P-value 0.020

Lags 0

-------------------------------------Trend: Constant

Critical Values: -3.46 (1%), -2.87 (5%), -2.57 (10%)

Null Hypothesis: The process contains a unit root.

Alternative Hypothesis: The process is weakly stationary.

mu=np.mean(spreadf)

sd=np.std(spreadf)

#设定交易期tradeStart='2015-01-01'

tradeEnd='2015-06-30'

PAt=PA[tradeStart:tradeEnd]

PBt=PB[tradeStart:tradeEnd]

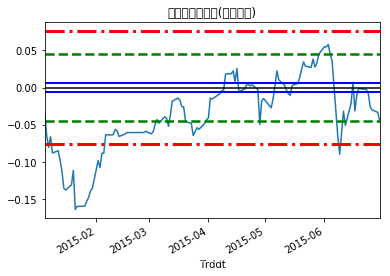

CoSpreadT=np.log(PBt)-beta*np.log(PAt)-alpha

CoSpreadT.describe()

count 119.000000

mean -0.037295

std 0.052204

min -0.163903

25% -0.063038

50% -0.033336

75% 0.000503

max 0.057989

dtype: float64

CoSpreadT.plot()

plt.title('交易期价差序列(协整配对)')

plt.axhline(y=mu,color='black')

plt.axhline(y=mu+0.2*sd,color='blue',ls='-',lw=2)

plt.axhline(y=mu-0.2*sd,color='blue',ls='-',lw=2)

plt.axhline(y=mu+1.5*sd,color='green',ls='--',lw=2.5)

plt.axhline(y=mu-1.5*sd,color='green',ls='--',lw=2.5)

plt.axhline(y=mu+2.5*sd,color='red',ls='-.',lw=3)

plt.axhline(y=mu-2.5*sd,color='red',ls='-.',lw=3)

<matplotlib.lines.Line2D at 0x1c2431b470>

level=(float('-inf'),mu-2.5*sd,mu-1.5*sd,mu-0.2*sd,mu+0.2*sd,mu+1.5*sd,mu+2.5*sd,float('inf'))

prcLevel=pd.cut(CoSpreadT,level,labels=False)-3

prcLevel.head()

Trddt

2015-01-05 -1

2015-01-06 -2

2015-01-07 -3

2015-01-08 -2

2015-01-09 -3

dtype: int64

def TradeSig(prcLevel):n=len(prcLevel)signal=np.zeros(n)for i in range(1,n):#反向建仓if prcLevel[i-1]==1 and prcLevel[i]==2:signal[i]=-2#反向平仓elif prcLevel[i-1]==1 and prcLevel[i]==0:signal[i]=2#强制平仓elif prcLevel[i-1]==2 and prcLevel[i]==3:signal[i]=3#正向建仓elif prcLevel[i-1]==-1 and prcLevel[i]==-2:signal[i]=1#正向平仓elif prcLevel[i-1]==-1 and prcLevel[i]==0:signal[i]=-1#强制平仓elif prcLevel[i-1]==-2 and prcLevel[i]==-3:signal[i]=-3return(signal)

signal=TradeSig(prcLevel)

position=[signal[0]]

ns=len(signal)

for i in range(1,ns):position.append(position[-1])#正向建仓if signal[i]==1:position[i]=1#反向建仓elif signal[i]==-2:position[i]=-1#正向平仓elif signal[i]==-1 and position[i-1]==1:position[i]=0#反向平仓elif signal[i]==2 and position[i-1]==-1:position[i]=0#强制平仓elif signal[i]==3:position[i]=0elif signal[i]==-3:position[i]=0

position=pd.Series(position,index=CoSpreadT.index)

position.tail()

Trddt

2015-06-24 0.0

2015-06-25 0.0

2015-06-26 0.0

2015-06-29 0.0

2015-06-30 0.0

dtype: float64

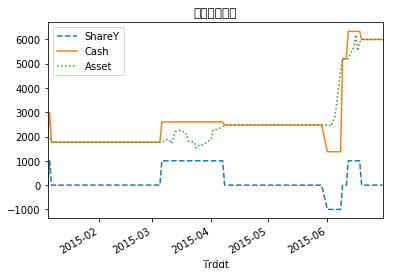

def TradeSim(priceX,priceY,position):n=len(position)size=1000shareY=size*positionshareX=[(-beta)*shareY[0]*priceY[0]/priceX[0]]cash=[2000]for i in range(1,n):shareX.append(shareX[i-1])cash.append(cash[i-1])if position[i-1]==0 and position[i]==1:shareX[i]=(-beta)*shareY[i]*priceY[i]/priceX[i]cash[i]=cash[i-1]-(shareY[i]*priceY[i]+shareX[i]*priceX[i])elif position[i-1]==0 and position[i]==-1:shareX[i]=(-beta)*shareY[i]*priceY[i]/priceX[i]cash[i]=cash[i-1]-(shareY[i]*priceY[i]+shareX[i]*priceX[i])elif position[i-1]==1 and position[i]==0:shareX[i]=0cash[i]=cash[i-1]+(shareY[i-1]*priceY[i]+shareX[i-1]*priceX[i])elif position[i-1]==-1 and position[i]==0:shareX[i]=0cash[i]=cash[i-1]+(shareY[i-1]*priceY[i]+shareX[i-1]*priceX[i])cash = pd.Series(cash,index=position.index)shareY=pd.Series(shareY,index=position.index)shareX=pd.Series(shareX,index=position.index)asset=cash+shareY*priceY+shareX*priceXaccount=pd.DataFrame({'Position':position,'ShareY':shareY,'ShareX':shareX,'Cash':cash,'Asset':asset})return(account)

account=TradeSim(PAt,PBt,position)

account.tail() | Position | ShareY | ShareX | Cash | Asset | |

|---|---|---|---|---|---|

| Trddt | |||||

| 2015-06-24 | 0.0 | 0.0 | 0.0 | 5992.514 | 5992.514 |

| 2015-06-25 | 0.0 | 0.0 | 0.0 | 5992.514 | 5992.514 |

| 2015-06-26 | 0.0 | 0.0 | 0.0 | 5992.514 | 5992.514 |

| 2015-06-29 | 0.0 | 0.0 | 0.0 | 5992.514 | 5992.514 |

| 2015-06-30 | 0.0 | 0.0 | 0.0 | 5992.514 | 5992.514 |

account.iloc[:,[1,3,4]].plot(style=['--','-',':'])

plt.title('配对交易账户')

Text(0.5, 1.0, '配对交易账户')

![CSS透明度[简述]](https://img-blog.csdnimg.cn/29730e6d4a244a93a08113d15ffa7665.png)