实证资产定价(Empirical asset pricing)已经发布于Github和Pypi. 包的具体用法(Documentation)博主将会陆续在CSDN中详细介绍,也可以通过Pypi直接查看。

Pypi: pip install --upgrade EAP

HomePage: EAP · Empirical Asset Pricing

Github: GitHub - whyecofiliter/EAP: empirical asset pricing

欢迎点赞、收藏、转发三连击!!!

————————————————

Fama-Macbeth 回归是实证资产定价中常用的实证方法。它用于验证因子是否具有显著的风险回报,具体内容可见实证资产系列文章中的Fama-Macbeth回归介绍。

我们添加了对回归得到的风险回报的图形化显示功能。具体函数为

def plot(self, figsize=(14, 7), together=False, window=None, select=None, **kwargs):

This function plots the regression slopes of the FM regression.

input :

figsize (tuple) : Figsize.

together (boolean) : Whether print the slope in one figure.

window (int) : The window of moving average slopes.

select (list) : Only print the selected slopes

函数的输入参数为

figsize:图像大小

together: 是否将风险回报画在一张图上

window:对风险回报进行移动平均处理,window为移动平均的窗口

select:只显示被选择变量的风险回报

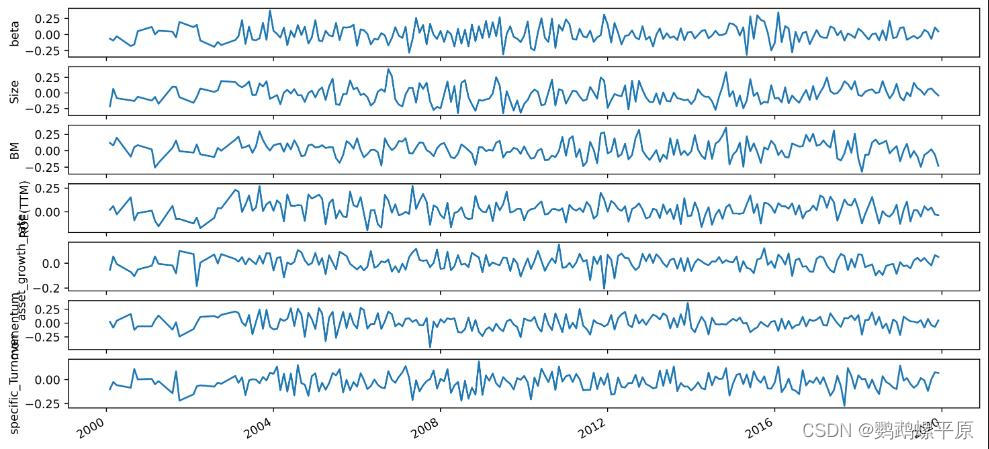

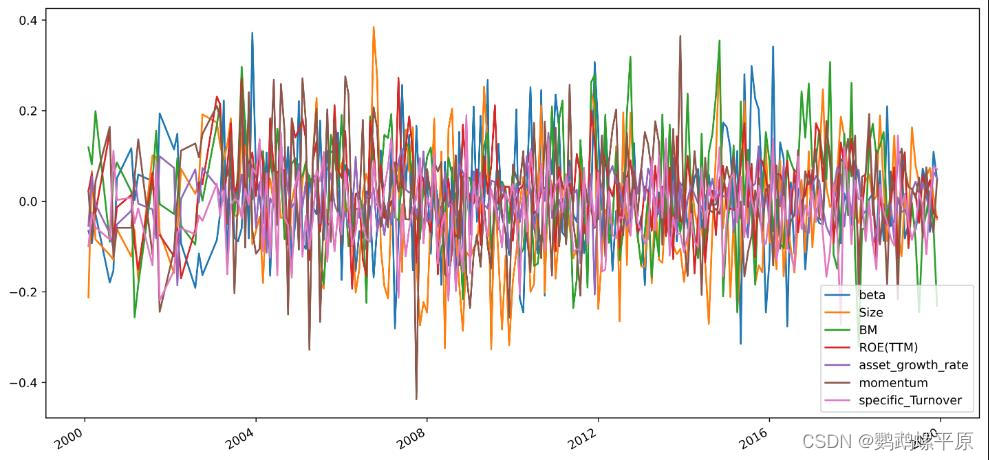

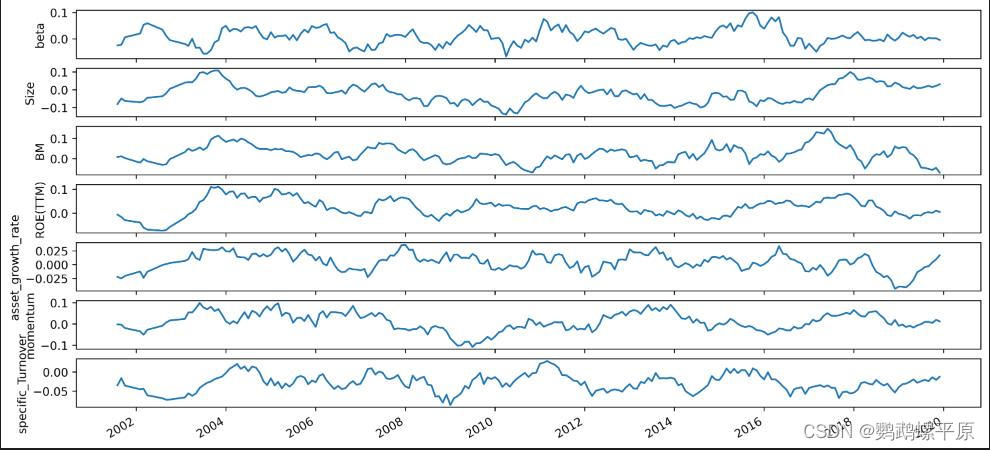

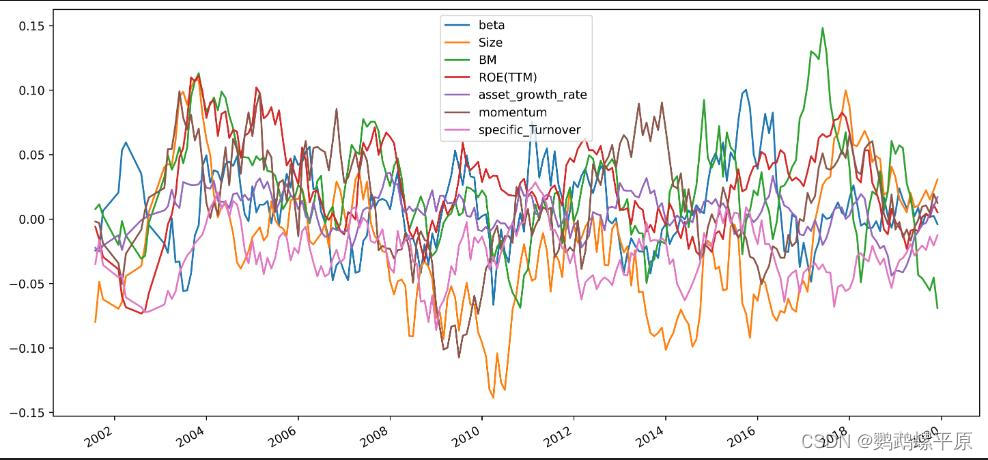

应用举例

from fama_macbeth import Fama_macbeth_regress as fmrmodel = fmr(sample)

model.fit()

model.plot(together=True, window=10)实际效果

![[MATLAB]一元线性回归(regress参数检验说明)](https://img-blog.csdnimg.cn/20200331164710650.png?x-oss-process=image/watermark,type_ZmFuZ3poZW5naGVpdGk,shadow_10,text_aHR0cHM6Ly9ibG9nLmNzZG4ubmV0L20wXzM3MTQ5MDYy,size_16,color_FFFFFF,t_70)